Table of Contents

Table of Contents

Introduction

Economic Strengthening is the basis for Rural Growth and Prime Minister Kisan Credit Card Yojana is the crucial move in realizing this dream. In India, with the increasing cost of farming as well as the variations in the climate patterns, credit on time has been a crucial link for the farmers. The scheme fills this gap, by providing liquidity and funding for the purchase of seeds, fertilizers, farm implements and other inputs. It’s the loans, certainly, but it’s more than that, too: About adding dignity to financial inclusion, lowering the distressed miles that women have to walk to access cash, and instigating sustainable agrarian growth.

What is Prime Minister Kisan Credit Card Yojana?

The Prime Minister Kisan Credit Card Yojana is an extension of the (erstwhile) Kisan Credit Card (KCC) scheme introduced in 1998. The KCC programme was tailored for providing short-term agriculture loans, but the PM-KCC Yojana introduces higher credit limit, added interest subsidy, and insurance for activities related to allied sectors such as dairy, fisheries, and animal husbandry. This is over and above the PM-KISAN direct income support scheme and is a model sui generis that would meet the credit and developmental needs of farmers in a cohesive manner, taking care of crops, credit, insurance and income support with a thrust on facilitating higher credit limit to farmers, in the long run and maturity period of 5 years.

Objectives of Prime Minister Kisan Credit Card Yojana

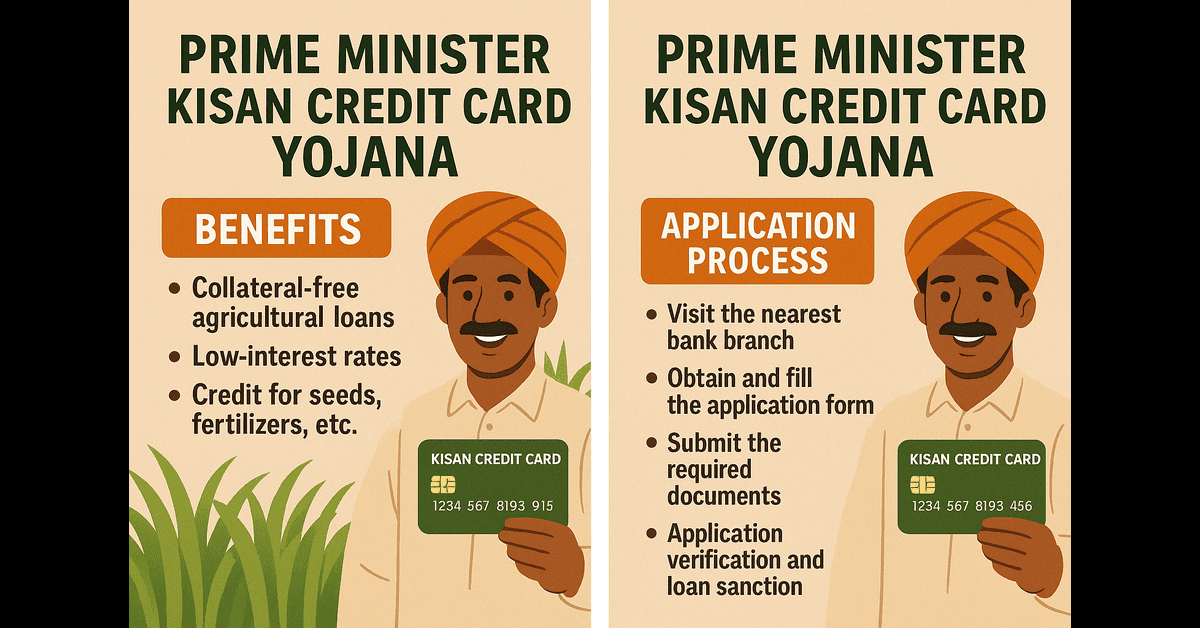

- Ensuring Credit Availability: Timely availability of credit at affordable interest rates to meet farmers’ cultivation cycle needs.

- Reducing Informal Lending: Curtailing dependency on moneylenders by offering formal financing options.

- Promoting Allied Activities: Expanding beyond crop cultivation to include dairy, poultry, fishery, and agro-processing.

- Supporting Small & Marginal Farmers: Tailored benefits, such as increased credit limit and waivers, to uplift vulnerable farmer segments.

Eligibility Criteria for Prime Minister Kisan Credit Card Yojana

Farmer Categories:

- Land-owning farmers cultivating agricultural/horticultural crops.

- Occupants and tenant farmers, based on state-level policies.

- For allied activities, individuals, SHGs, or clusters engaging in dairy, fishery, etc., are eligible.

Documentation Requirements:

- Identity proof (Aadhaar, PAN or voter ID).

- Land ownership certificate or cultivation proof.

- Passport-sized photos and contact information.

- Letter of recommendation or self-declaration for tenant farmers/SHGs.

Application Process for Prime Minister Kisan Credit Card Yojana

Offline Method:

Visit the nearest bank branch with documents. Submit the KCC application form along with photocopies of documents. Banks will assess eligibility, decide credit limit, and sanction the card.

Online Method:

Available through many banks’ online portals and government cowintegration platforms. Farmers can upload scanned documents, sign digitally, and receive approval without visiting the bank.

Bank and Institutional Role:

Public, RRBs, PACS, and select private banks are all involved. They offer sanction, disbursement, interest subsidies, and insurance coverage.

How To Apply For PM Kisan Credit Card Online?

Loan Limit and Interest Rates under Prime Minister Kisan Credit Card Yojana

Credit Limit Framework:

- Up to ₹3 lakh for crops and allied activities.

- Tiered limits: Marginal farmers (≤2 ha): ₹1–1.6 lakh, Small farmers (2–5 ha): ₹1.6–3 lakh

- Beneficiaries of PM-KISAN can access a loan of ₹10,000 over the regular limit for seasonal needs.

Interest Rate & Subsidies:

Farmers receive loans at a concessional rate of 4–7% per annum. Eligible borrowers benefit from up to 2% interest subsidy if repayment is made within due time.

Repayment Structure:

Aligned with crop cycles. Usually one-year tenor, extendable depending on crop duration or allied activity nature.

Key Benefits of Prime Minister Kisan Credit Card Yojana

- Timely Liquidity: Farmers access funds quickly for sowing and cultivation inputs.

- Cost-Benefit: Lower interest rates and subsidy funding significantly reduce financial burden.

- Multi-purpose Utility: Covers cultivation, allied activities, and working capital needs.

- Insurance Protection: KCC is coupled with accident and crop insurance, safeguarding farmers and their families.

- Ease of Use: Card facility with ATM/debit access adds convenience and transparency.

Digital Kisan Credit Card: Latest Updates

The Digital Kisan Credit Card is an additional innovation that makes use of digital signatures, e-KYC, and UPI. Through mobile devices, farmers can monitor transactions, view subsidy credits, get alerts, and withdraw money, cutting down on delays and boosting accountability. Prime Minister Kisan Credit Card Yojana

Challenges in Implementation

- Problems with Awareness: Underutilization results from a lack of knowledge about eligibility and benefits.

- Disbursement Delays: Documentation obstacles and conventional banking procedures cause delays in sanction.

- Finalization Delays: Schedule delays and policy misalignment occur in some remote areas.

- Inclusion of Marginal Farmers: Tenant cultivators in particular continue to face obstacles, as do many smallholder farmers.

श्रम कार्ड से ₹3000 कैसे मिलेंगे:

Success Stories: Farmers Benefiting from the Scheme

- A progressive Punjab farmer used the KCC loan to invest in drip irrigation, leading to a 25% productivity gain.

- A woman-led dairy cluster in Maharashtra accessed KCC funds to scale operations, uplift income, and empower women in a rural setting.

Comparative Analysis with Other Schemes

- NABARD Schemes vs KCC: While NABARD provides long-term infrastructure credit, KCC offers short-term working capital.

- PMFBY vs KCC: Crop Insurance is a risk buffer; KCC is liquidity support. Together, they form a comprehensive safety net. Prime Minister Kisan Credit Card Yojana

Role of RBI and NABARD

To ensure regulatory alignment and financial discipline, the RBI establishes prudent standards and NABARD oversees their implementation through cooperative and rural banks.

Effect on the Productivity of Agriculture

Loans from KCC make it possible to buy seeds, fertilizer, and equipment on time, which boosts crop yields, increases sowing areas, and improves farm returns. Prime Minister Kisan Credit Card Yojana

Empowerment of Women through the PM-KCC Yojana

Targeted benefits for women farmers include higher interest concessions and the opportunity to join SHGs and clusters, which promotes gender parity in credit availability and self-reliance.

Sustainable Farming and Its Effect on the Environment

Sustainable agriculture and climate adaptation depend on environmentally friendly investments like solar pumps, microirrigation, and organic farming, which are supported by KCC funds.

Steps to Improve the Scheme

- Enhance awareness via village workshops and digital campaigns.

- Streamline online KCC applications.

- Strengthen database linkages with DBT, PM-KISAN, PMFBY, and soil health cards.

- Increase allotment for allied farmers.

- Add features like crop-linked digital credit history.

India’s Agricultural Finance Future

With AI-assisted pre-approved credit limits and integrated dashboards that connect credit, weather, market prices, soil data, and insurance for a strong agrifin model, the future is digital.

FAQs

Who is eligible to apply for PM-KCC Yojana?

Land-owning, tenant, or occupant farmers. Allied activity operators and SHGs are also eligible.

How can one apply for a Kisan Credit Card?

Visit a bank branch or apply online via banks’ portals; submit ID, land proof, and photograph.

What is the maximum loan amount?

Up to ₹3 lakh, depending on farming category and crop plan. Additional ₹10,000 for PM-KISAN beneficiaries.

What documents are needed?

Aadhaar, land ownership or cultivation proof, documents specific to allied activities, and photographs.

Is there any penalty for delayed payment?

Yes, penalty interest applies. However, timely repayment offers up to 2% subsidy concession.

Does the KCC come with insurance?

Yes, it includes personal accident and crop insurance as mandated by bank policies.

Conclusion:

The Prime Minister Kisan Credit Card Yojana is a historic step towards making the Indian farmer financially inclusive, creditworthy and also empowered. By connecting liquidity with productivity and sustainability this initiative fosters farm and allied sectors expansion and balanced growth. Further digital evolution, policy fine-tuning, and outreach can unlock its full potential, helping to forge a higher-skilled, empowered agricultural labor force.

नमस्ते मेरा नाम है (कमल विश्वकर्मा )और ये मेरी साइट है kamalblogging.in यहां आपको डेली न्यूज़ एंटरटेनमेंट और साथ ही अर्निंग टिप्स और हेल्थ से जुड़ी जानकारी मिलेगी | जिसे आप इंटरनेट पर ढूंढते हैं | अगर आप ब्लॉगिंग के दुनिया में करियर बनाना चाहते हैं तो इस ब्लॉग को सब्सक्राइब जरूर करें| धन्यवाद